I got a wakeup call on February 9th, 2017. It came in the form of an unexpected email from Nationwide. It read, “Hi Ryan. Your dad and I were talking about the car insurance this morning and he wants me to quote your 2002 Toyota Camry on its own policy for you.”

This was my dad’s tough love way of kicking me off the family insurance plan and I was pissed. Especially when I got the bill in the mail for $1,023.16. But it did help me learn an important life lesson… loyalty is overrated. Have you ever seen the Geico commercial claiming that “15 minutes can save you 15% or more on car insurance”? Well, it took a lot longer than 15 minutes but my record is 46%. By 2018, I’d dropped the comprehensive insurance on my aging car to get the premium down to $776 (24% savings), and then scored another 29% savings by switching to Erie at $552/year (which was down 46% from that original Nationwide bill).

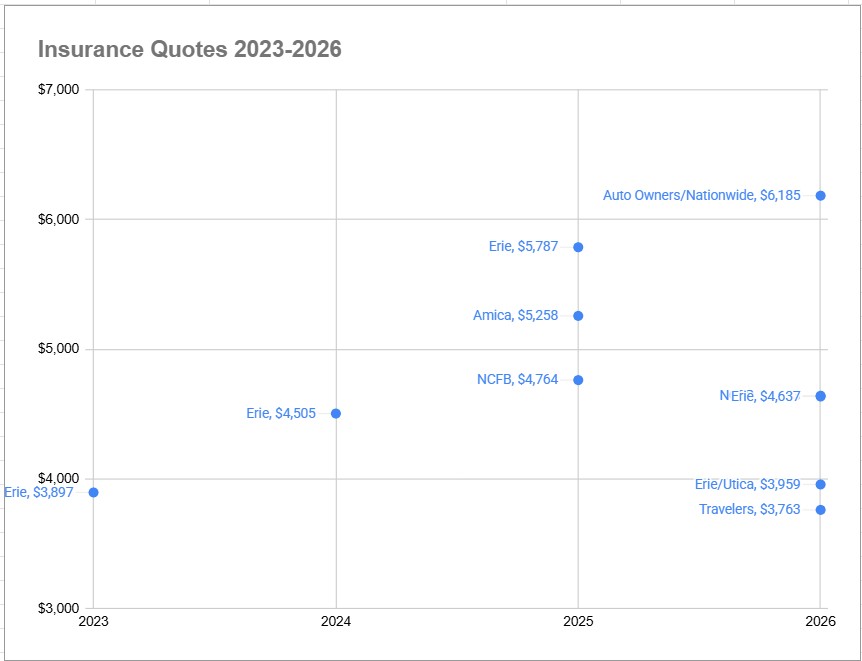

Over time, I’ve collected quotes from 13 different insurance carriers and changed companies three times. I know that seems ridiculous but then again between 2023 and 2025, my insurance bill with Erie went up by 48% ($3,897 to $5,787)! Just the homeowners portion of the bill was up 77% over that two year period. I pressed my agent on this and she forwarded a canned message from Erie corporate. It read (in part), “There is no way to sugarcoat that this is going to be the most challenging period we have seen with regard to personal auto and home insurance.” Whatever. I switched to NC Farm Bureau to save $1,023 (18%).

My rate with NC Farm Bureau actually went slightly down between 2025 and 2026 ($4,763 to $4,643) but it still never hurts to test the market. One particularly honest agent sent me a candid note, “Currently, I do not have a competitive quote to offer or recommend switching from your current carrier…” Thankfully my friend (and now agent) Zach helped me to find a split policy (Erie for auto, Utica for homeowners) that actually provides better coverage than my prior policy, while still saving $684 (15%).

A few lessons learned as a consumer:

- Check with an independent broker (or two) who can shop multiple carriers on your behalf. Shopping for quotes is hard… It typically requires picking up the phone, figuring out how to make an apples to apples comparison for different policies, and then ending up on a spam list. A good broker can do this heavy lifting on your behalf. Want to borrow mine? Reach out to zach.routh@allchoiceinsurance.com.

- Track your data! My goal is to pay the full premium up front, not think about insurance for a year, and then keep a record in a Google folder of how it changed since last year. Don’t put it on auto-pay, otherwise you might get complacent and just let it auto-renew.

- You don’t have to keep your auto and homeowners policies with the same company if bundling isn’t actually saving you money. For example, splitting coverage (like using Erie for auto and Utica for homeowners) can sometimes provide better overall coverage while still saving you money.

- Don’t skimp on the liability coverage just to lower your bill. For example, I could deal with a slightly higher deductible but it’d be a lot tougher to recover from a $1,000,000 lawsuit.

- Disclaimer… Insurance isn’t a commodity so you need to be careful about what you’re signing up for. When comparing different proposals, I’ll read the policy (including the riders), check their reputation via Consumer Reports, Reddit, and a general web search, and review the Company’s AM Best rating, which rates the financial health of the company. And aside from the coverage numbers highlighted on the quote, you need to understand what’s covered and what isn’t. That can make a big difference! With the most recent switch, I upgraded from an HO-3 policy (Farm Bureau) to an HE-7 policy (Utica). An HO-3 will cover all “named perils” like a fire, theft, or hail, whereas an HE-7 will cover any accidental loss unless it’s specifically excluded. So just as a wild example, if a raccoon broke into my house and tore up all my furniture, I’m covered under the HE-7 (subject to a $2,500 deductible).

A few lessons from Zach, a friend and independent agent (that doesn’t work off commission):

- If you can afford it, raise your deductibles. Then put aside the amount of the deductible in an emergency/rainy day fund, so you have that money on hand if something were to happen. Upping your deductible will likely significantly lower your rate.

- Read your policy and make sure your information is correct. It can sometimes saves some extra cash, but most importantly, you know your needs way better than any agent or carrier, and you don’t want to be up a creek in a claims situation because you didn’t check the details.

- State minimum liability requirements terrify me. North Carolina increased the requirements for automobile liability coverage in the summer of 2025. However, having the minimum is exactly what it sounds like. $50,000 of Property Damage Coverage seems hefty until you consider that $50,000 is basically the average cost of a new car these days. If you are wondering why I recommend $250,000/$500,000 for Bodily Injury Coverage, take a second to think about where all the money comes from to plaster injury attorney advertisements on our billboards and televisions.

- Ask an agent. Sure, you can acquire insurance in minutes on your phone, and it might save you money. But there is a tremendous value to working with a local insurance professional who is invested in your well-being rather than a bottom line.

- Talk to an agent before you file a claim. Insurance companies can drop you for claims experience (or raise your rates), so before you file, make sure doing so is in your best interest.